Many Singaporeans enjoy company health insurance as part of their employee benefits, but how many know exactly what is covered?

If you have ever wondered how your corporate health insurance works, what it pays for, or what happens when you leave your job, you are not alone.

This guide breaks down the essentials in a clear and practical way, so you can better understand your coverage and avoid unexpected costs.

What is corporate health insurance?

In Singapore, corporate health insurance is also commonly referred to as Group Hospital & Surgical (GHS).

Think of it as a master policy your employer buys on your behalf. This means you don't actually own it; the company does.

Your eligibility typically depends on you being actively at work, and how much coverage you get largely comes down to what your employer has decided to spend on it.

What does corporate health insurance in Singapore typically cover?

Corporate health insurance in Singapore typically bundles several types of coverage together, though what you actually get depends on the plan your employer has chosen. Here is a breakdown of the most common benefits.

Inpatient / hospitalisation benefits

Most plans set a daily limit on what they will pay for your hospital room, typically somewhere between $200 to $500 per day. If you choose a room that costs more than that, you foot the difference yourself.

Surgical costs are also capped. For example, if your insurance plan covers $5,000 and your bill totals $15,000, you are responsible for paying the remaining $10,000.

Outpatient benefits

Many corporate plans give you access to a network of panel clinics where you can see a GP without paying out of pocket. Just show your staff card or e-card at the front desk. Depending on the plan your employer bought, you may still need to pay a small co-payment, so it is worth checking with HR beforehand.

If you need to see a specialist, most plans require you to visit a panel GP first and get a referral before the specialist consultation is claimable. Skipping this step usually means the cost falls on you.

Planning to see a specialist? Browse Thomson Medical's specialist directory to find the right doctor for you.

Dental and optical benefits

These are usually optional add-ons that your employer may or may not include. Where they do exist, they tend to cover the basics like routine scaling and polishing, or a fixed allowance toward glasses or contact lenses.

Maternity benefits

Not all corporate plans include maternity coverage, so it is worth checking early, especially if you are planning to start a family. Where it is included, there is usually a schedule that spells out exactly how much is claimable for pre-natal checkups and delivery.

In many cases, corporate plans cover only part of maternity-related costs, so it is helpful to review your benefits early if you are planning a family.

Planning to deliver at Thomson Medical? Check out our maternity packages or get in touch with our medical concierge team to find out more.

Mental health coverage

More employers are starting to include mental health benefits, which is a positive shift. That said, coverage is often limited to inpatient psychiatric care, and many plans have a waiting period of around 10 months before you can make a claim for mental health-related hospitalisation.

.png?branch=production)

What is usually not covered under corporate health insurance

Every corporate plan has its limits. Understanding these helps you avoid unexpected costs. Here are some of the most common exclusions to look out for.

Pre-existing conditions

This is the most significant gap in most corporate plans. If you had a medical condition before joining the company, your GHS plan will likely not cover treatment related to it.

Some employers do manage to negotiate a waiver of pre-existing conditions with their insurer. This is more common in larger companies where the insurer is covering a big enough group to spread the risk. If you are unsure whether your plan includes this, it is worth checking with HR directly.

Elective and cosmetic procedures

If a procedure is not medically necessary, it generally will not be covered. Braces are a common example. Orthodontic treatment is almost universally excluded from corporate plans in Singapore unless it was required as a result of an accidental injury at work.

Overseas treatment

If you choose to seek treatment abroad, most plans will only reimburse you based on what the equivalent treatment would have cost at a Singapore public hospital. Anything above that comes out of your own pocket.

How to use your corporate health insurance in Singapore

There are a few different ways to use your corporate health insurance, depending on the situation.

For everyday GP visits, the easiest route is to find a panel clinic through your insurer's app, show your e-card at the front desk, and pay a small co-payment, and the rest is billed directly to your insurer.

If you choose to see a doctor outside the panel network, you will need to pay the full bill upfront and submit a reimbursement claim afterwards. Just be aware that non-panel claims are often reimbursed at a lower rate, so you may not get back everything you paid.

For hospital stays, your insurer can issue a Letter of Guarantee (LOG) directly to the hospital. This means you will not need to put down a large cash deposit upon admission, a small but significant relief when you are already dealing with hospitalisation.

Being admitted to Thomson Medical? Contact our medical concierge team and we will help arrange your Letter of Guarantee before you arrive.

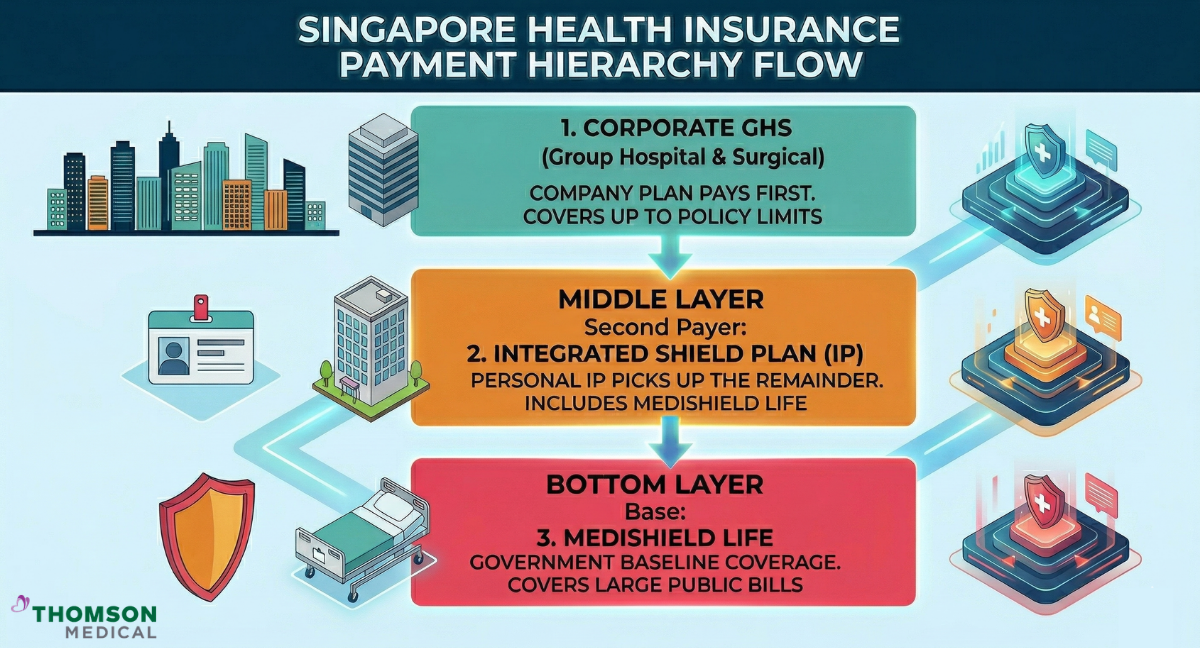

Corporate Insurance vs. MediShield Life vs. IP: How they work together

Understanding how your different insurance policies interact can make a real difference to how much you end up paying out of pocket. In Singapore, there is a specific claims hierarchy that determines which policy pays first when you are hospitalised.

Your corporate GHS plan pays first

When you are admitted to hospital, present your corporate insurance details first. The hospital will bill your corporate insurer for as much of the cost as your policy limits allow.

Your Integrated Shield Plan and MediShield Life picks up the remainder

If your bill exceeds what your corporate plan covers, which can happen with major surgeries or stays in private hospitals, your personal Integrated Shield Plan (IP) steps in to cover the balance.

MediShield Life is already bundled into your IP, so you do not need to think about it separately.

Can I use my corporate health insurance and IP together?

One thing many employees do not realise is that having both a corporate plan and a private IP can significantly reduce what you pay at a private hospital. Most IPs come with a deductible (typically $3,500) and a co-insurance component of around 10% of the remaining bill. These are costs you would normally pay in cash.

By using your corporate plan to absorb the deductible and co-insurance, you can effectively reduce your out-of-pocket costs to near zero, even at a private hospital. This means you can access the specialist of your choice without having to dip into your savings. This combination can significantly reduce your out-of-pocket costs.

Want to understand how your corporate plan and IP work together at Thomson Medical? Get in touch with our team and we will walk you through it.

Factors that affect your corporate coverage

Not all corporate health plans are created equal. Even within the same company, what you are covered for can vary depending on a handful of factors that are easy to overlook until you actually need to make a claim.

Ward class and pro-ration

This is one of the most common sources of bill shock. If your corporate plan is pegged to a Class C ward but you choose a private room, your insurer will only pay a proportion of the bill, sometimes as little as 50%. The rest comes out of your pocket. Before you get admitted, it is worth finding out exactly what ward class your plan covers.

Per disability vs. annual limits

These two terms determine how far your coverage actually stretches.

Per disability limit

Resets for each new condition.

If your plan covers $10,000 per disability, you get $10,000 for a knee surgery and another $10,000 if you are hospitalised for something unrelated later.

Annual limit

A hard ceiling for the entire year across all claims. Once you hit it, you are on your own for the rest of the year.

When comparing plans or asking HR about your coverage, knowing which type of limit applies can help you avoid a nasty surprise mid-year.

What happens to your coverage when you leave your job?

Your corporate coverage typically ends on your last day of employment.

This creates a few risks that are easy to overlook:

If you fall ill while between jobs, you have no coverage.

If you are diagnosed with something new during that gap, your next employer's plan may classify it as a pre-existing condition and exclude it entirely.

This is one of the strongest arguments for having a personal IP that you own regardless of where you work.

Tips for making the most of your corporate health benefits

Know what ward class your plan is pegged to. It directly affects how much you pay out of pocket.

If you have a personal IP, use your corporate plan's Letter of Guarantee to get admitted to a private hospital like Thomson Medical, where your corporate plan absorbs the upfront costs your IP would otherwise require you to pay.

And always keep a copy of your Schedule of Benefits somewhere accessible, even after you leave the company.

Your corporate health insurance is most valuable when you understand it before you need it. If you are planning a hospital stay or specialist consultation at Thomson Medical, get in touch with our medical concierge and we will help you navigate your coverage.

FAQ

If I leave my job, does my corporate insurance stop immediately?

Yes. Coverage under a Group Hospital & Surgical (GHS) policy typically ends on your last day of employment. Since the employer owns the policy, the benefit is tied to your status as an active employee. This can leave you vulnerable to pre-existing condition exclusions if you try to buy a new personal policy after your health has already changed.

Should I claim my corporate insurance or personal insurance?

Claim corporate insurance first. In Singapore’s claims hierarchy, GHS is the primary payer. Using your employer's plan first allows it to extinguish the deductible (the first $3,500) and co-insurance (10%) of your personal Integrated Shield Plan (IP). This strategy can result in near-zero out-of-pocket costs at private hospitals like Thomson Medical.

If I’m covered under my employer’s group insurance, can I still claim from MediShield Life?

Yes, but only for the balance. Singapore follows the indemnity principle, which prevents you from double claiming or profiting. If your corporate plan hits its limit, your IP or MediShield Life will step in to cover the remaining costs. Your IP insurer usually coordinates the claims process automatically so you don't have to file separate claims.

What is the difference between Compulsory and Voluntary corporate plans?

A compulsory (non-contributory) plan covers all eligible employees automatically, with the employer paying the full premium. A voluntary (contributory) plan allows employees to choose whether to participate, often requiring them to pay a portion of the insurance premiums themselves. Both types may still involve a co-payment at the point of service depending on the specific policy design.

In what order should I use my different insurance plans?

Singapore follows a coordination of benefits principle to ensure you don't profit from a claim. Typically, your employer’s GHS plan pays first as the primary coverage. If the bill exceeds those limits, your Integrated Shield Plan (IP) kicks in to cover the remainder. MediShield Life serves as the ultimate baseline layer, and if you have an IP, your private insurer handles both the IP and MediShield Life components together for you.

Can I use my corporate insurance to cover my personal IP's deductible?

Yes, this is a highly effective strategy. Most personal IPs require you to pay a deductible (the first $3,500) and a co-insurance (usually 10%) out of pocket. However, if your corporate GHS plan covers these initial costs, it effectively extinguishes your personal financial obligation. This allows you to stay at a private hospital like Thomson Medical with potentially near-zero cash outlay.

Am I covered immediately after joining a new company?

Coverage usually depends on an actively-at-work clause. This means you must be physically at work and capable of performing your duties on the day the policy commences to be eligible for coverage. If you are on medical leave on the start date, your coverage may be deferred until you return to work. However, once active, most plans waive waiting periods for accidental injuries.

Are pre-existing conditions covered under corporate plans?

While MediShield Life covers pre-existing conditions for all Singaporeans, most corporate GHS and private IP plans exclude them by default. However, some large corporate groups may negotiate a waiver of pre-existing conditions, meaning you are covered for past illnesses immediately upon joining. You should check your specific schedule of benefits to see if this waiver applies to you.

Do I need a referral to see a specialist?

To ensure your specialist consultation is claimable under most managed healthcare or GHS plans, you generally must obtain a referral from a panel GP first. The GP acts as a gatekeeper to ensure the treatment is medically necessary. If you visit a specialist without this referral, your insurer may reject the claim or reimburse you at a significantly lower rate.

How does my choice of hospital ward affect my claim?

Your plan is usually pegged to a specific ward class (e.g., Government Class B1). If you choose a higher ward or a private hospital like Thomson Medical, a pro-ration factor is applied. This means the insurer will only pay a percentage of the bill (e.g., 50% or 65%), and you or your Integrated Shield Plan will have to cover the substantial gap created by the ward upgrade.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, medical, or legal advice. Thomson Medical does not earn any commission, referral fees, or financial benefit from any insurance products or providers mentioned in this article. All information is provided purely to help you better understand Singapore's health insurance landscape.

Individual circumstances vary, and the right insurance plan depends on your personal health profile, financial situation, and coverage needs. Before making any decisions about your health insurance, we strongly recommend speaking with a licensed financial adviser or your insurance provider directly.

For more information, contact us:

Thomson Medical Concierge

- 8.30am - 5.30pm

- WhatsApp: 9147 2051

Need help finding the right specialist or booking for a group?

Our Medical Concierge is here to help you. Simply fill in our form, and we'll check and connect you with the right specialist promptly.

Notice:

The range of services may vary between Thomson clinic locations. Please contact your preferred branch directly to enquire about the current availability.

Get In Touch