Healthcare in Singapore is among the best in the world, but it can also be expensive. Even a routine GP visit may cost more than SGD 50, while hospital treatment can quickly reach tens of thousands of dollars.

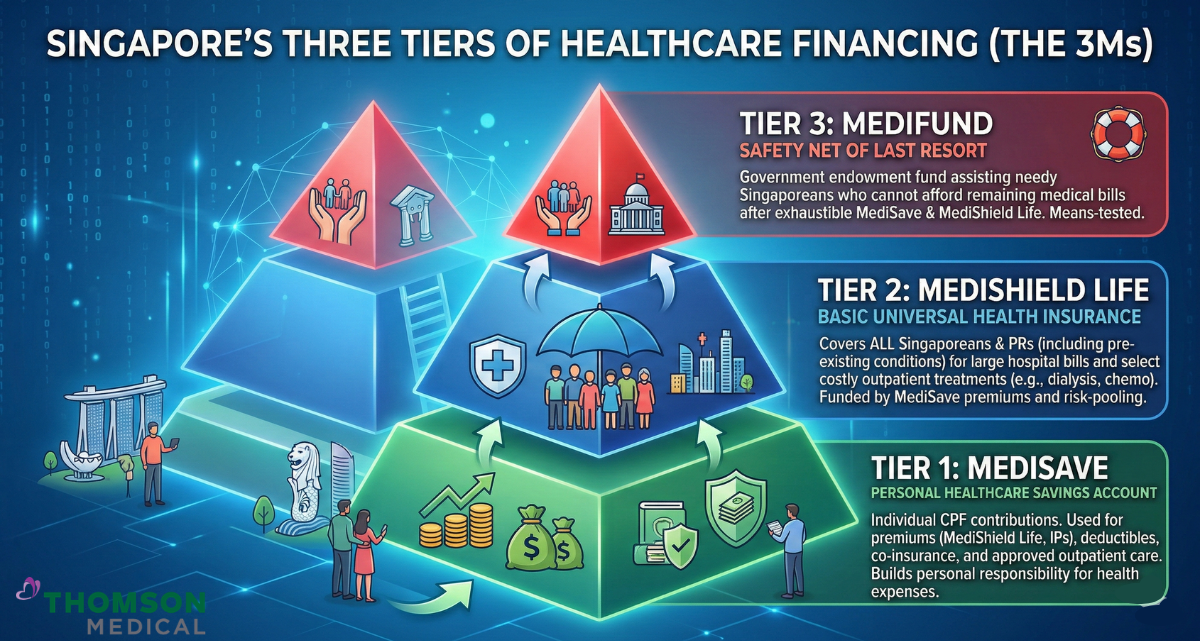

Most Singaporeans are covered by MediShield Life, MediSave and MediFund, the 3 pillars of Singapore’s health financing scheme. However, many people discover that governmental schemes alone do not cover the full cost of private healthcare or higher ward classes.

Understanding how Singapore’s health insurance system works can help you make better decisions about your coverage. When you know what your existing insurance pays for and where the gaps are, it becomes much easier to decide whether an integrated shield plan or IP rider is worth considering.

What’s the difference between MediShield Life, MediSave and MediFund?

Most people know they are covered by "something" when it comes to healthcare in Singapore but very few can explain exactly what that something is.

The government's support does not come as a single scheme. It is three separate programmes, each serving a distinct purpose, and knowing what each one does will tell you a lot about where your coverage actually stands right now.

MediSave

MediSave is not an insurance plan. It is a personal medical savings account within your CPF. Each month, part of your CPF contribution goes into MediSave.

MediSave can pay for:

Hospitalisation

Day surgery

Certain outpatient treatments

Health insurance premiums like MediShield Life and Integrated Shield Plans

The medical expenses of your immediate family members

Think of MediSave as the account that helps cover healthcare costs that insurance does not fully pay for.

MediShield Life

MediShield Life is Singapore’s national health insurance scheme. It is run by the Central Provident Fund (CPF) Board and automatically covers all Singapore Citizens and Permanent Residents, including those with pre-existing medical conditions.

Its purpose is to help pay for large hospital bills and certain costly outpatient treatments such as chemotherapy or dialysis.

However, MediShield Life coverage is designed around subsidised B2 and C wards in public hospitals. If you choose a higher ward class or a private hospital, the amount covered will be lower compared to the total bill.

Premiums for MediShield Life are paid using your MediSave account directly and gradually increase as you age.

MediFund

MediFund acts as the final safety net in Singapore’s healthcare system. It supports Singapore Citizens who are unable to afford their medical bills even after MediShield Life coverage and MediSave savings have been used.

Unlike MediSave or MediShield Life, MediFund is not something you sign up for in advance. Patients typically apply through a medical social worker at a public hospital if they face financial difficulty paying their medical bills. Eligibility is assessed based on financial need at the time of application.

Summary of governmental healthcare financing schemes | |||

|---|---|---|---|

What it is | What it covers | How you pay for it | |

MediSave | Personal healthcare savings account within your CPF |

| Funded automatically via monthly CPF contributions |

MediShield Life | National health insurance scheme for ALL Citizens and PRs. (Including people with pre-exsisting conditions) | Large hospital bills and costly outpatient treatments. Benchmarked to B2/C ward rates. | Paid from MediSave. |

MediFund | Government safety net for those who cannot afford remaining bills. | Residual bills after MediShield Life and MediSave have been applied. | No premium. Apply via a medical social worker at a public hospital. |

When is private insurance necessary?

MediShield Life provides important baseline coverage, but it was designed mainly for treatment in subsidised wards in public hospitals.

If you prefer treatment in a Class A or B1 ward, or at a private hospital, MediShield Life will only cover a portion of the bill (between 10% to 16%), and the exact amount will be subject to strict MediShield Life claim limits.

For example, a major surgery such as a total knee replacement in a private hospital may cost between SGD 35,000 and SGD 50,000. MediShield Life may only cover a small part of that amount.

MediShield Life also DOES NOT fully cover certain pre- and post-hospitalisation costs, such as specialist consultations and diagnostic scans. This means that you need to consider not only whether you can afford a health insurance policy’s premiums but also any sudden out-of-pocket expenses if anything serious happens.

Types of health insurance plans

Singapore’s private health insurance market offers several different types of plans. Each plan is designed to protect against different financial risks.

Understanding how these plans work will help you decide which type of coverage may suit your needs.

Common types of private health insurance include:

Integrated Shield Plans (IP)

Hospitalisation and Surgical insurance

Critical Illness insurance

Personal Accident insurance

Group health insurance from employers

Below, we will discuss the above health insurance plans and go into detail on what sets them apart from each other.

Integrated Shield plans (IPs)

IPs are the most common form of private health insurance in Singapore, held by around 70% of residents. IPs stack on top of MediShield Life, extending your coverage so that you can choose treatment in:

Higher ward classes in public hospitals (Class A or B1)

Private hospitals

Your chosen IP plan tier determines where you can receive treatment and how much of your bill is covered by your insurer.

There are currently seven insurers offering IPs in Singapore:

AIA

Prudential

Great Eastern

HSBC Life

Singlife

Income

Raffles Health Insurance

Want to learn more about what an IP covers, what it doesn’t cover and its cost? Read our deep-dive on integrated shield plans here.

.png?branch=production)

Hospitalisation & Surgical (H&S) insurance

Hospitalisation and Surgical (H&S) insurance is designed to cover medical costs related to hospital stays and surgical procedures. Unlike Integrated Shield Plans, standalone H&S insurance is not linked to MediShield Life and cannot be paid using MediSave.

These plans are most commonly used by foreign residents who are not eligible for MediShield Life. For Singapore Citizens and Permanent Residents, IPs are usually the more practical option.

Critical Illness insurance (CI)

CI works differently from hospitalisation insurance.

Instead of paying your medical bills directly, it provides a lump sum payout when you are diagnosed with a covered serious illness such as cancer, heart attack or stroke.

You can use this payout for ANY purpose, including:

Medical treatment

Daily living expenses

Mortgage payments

Replacing lost income

Most standard CI plans only pay out when the illness reaches an advanced stage, while Early CI Plans pay out from the earlier stages of disease.

Learn about the 4 different types of critical illness policies in our article on hospitalisation insurance.

Personal Accident insurance (PA)

Personal Accident insurance covers injuries caused by accidents rather than illness.

Typical coverage includes:

Medical expenses for accident-related injuries

Compensation for permanent disability

Accidental death benefits

Some policies in Singapore also include protection against certain infectious diseases such as dengue, Hand, Foot and Mouth Disease, and food poisoning.

Personal Accident insurance is usually inexpensive and works best as an additional layer of protection alongside other health insurance plans.

Company health insurance / Group health insurance (GHS)

Many employers in Singapore provide group health insurance as part of their benefits package.

Company health insurance plans typically cover:

Outpatient GP visits

Specialist referrals

Hospitalisation

The limitation of company health insurance is that the group coverage is tied directly to your employment.

When you leave a job, your coverage stops, often immediately, and if you have developed a health condition during that period, securing your own individual plan afterwards may come with exclusions or higher premiums.

Riders and add-ons

A rider is an optional add-on that you can buy together with an Integrated Shield Plan. Its purpose is to reduce how much you pay out of pocket when you are hospitalised.

Without a rider, your Integrated Shield Plan still requires you to pay part of the bill yourself. This may include:

Deductibles, which is the amount you pay before the insurance starts paying

Co-insurance, which is a percentage of the remaining bill that you still need to cover

A rider helps reduce this burden by lowering or capping what you need to pay yourself each year.

It is also important to remember that rider premiums must be paid fully in cash. You cannot use MediSave for them. When reviewing a plan, it helps to look not just at the base premium but also at the total cost of the plan plus rider over time.

For a more detailed breakdown about what a rider is and explanations on how deductibles and co-insurance work, read our article on integrated shield plans.

Overview of health insurance plans in Singapore | ||

|---|---|---|

Plan type | What it covers | Best for |

Integrated Shield Plan (IP) | Provides coverage for higher ward classes and private hospitals. Partially MediSave-payable. | Most Singapore Citizens and PRs wanting coverage beyond B2/C wards. |

H&S Insurance | Standalone cover for hospital stays and surgery, not linked to MediShield Life and not payable via MediSave. | Foreign residents on Employment Passes not eligible for MediShield Life. |

Critical Illness (CI) | Pays a lump sum on diagnosis of serious conditions such as cancer. Payout is unrestricted, use it for anything. | Those who need income replacement or expense cover during prolonged recovery. |

Personal Accident (PA) | Covers accident-related medical costs, permanent disability, and accidental death. | Anyone wanting low-cost protection for risks not covered by an IP. |

Group Health Insurance (GHS) | Employer-provided cover for outpatient GP visits, specialist referrals, and hospitalisation. Scope varies by employer and ends when employment does. | Employees. |

Riders | Optional add-on to an IP that lowers or caps deductibles and co-insurance. Must be paid fully in cash. | IP holders who want lower out-of-pocket cost when hospitalised. |

Cost of health insurance in Singapore

Most people in Singapore pay for health insurance without fully knowing whether they are on the right plan, overpaying for coverage they do not need, or underinsured for the situations that actually matter.

This predicament is more common than you'd think and the good news is that once you understand what drives the cost of your premiums, you are in a much stronger position to make a decision based on your actual needs rather than on what you were sold.

Health insurance costs in Singapore vary based on a few main factors, including:

Age

The type of plan you choose

Ward class or hospital tier covered

Your current health

In general, premiums are lower when you are younger and rise gradually with age. Plans that cover private hospitals usually cost more than plans for public hospital wards. Because of this, two people can be paying very different premiums even if they are both insured.

A common mistake is to focus only on what a plan costs today. A plan that feels affordable in your 30s may become much more expensive in your 60s and 70s. It is worth choosing a level of coverage you can realistically sustain over the long term.

Before committing to a plan, you can use the official CPFB calculator to estimate both your MediSave usage and your cash outlay. This gives you a more realistic view of what the policy will cost year after year.

Using Medisave to pay premiums

One of the helpful features of Singapore’s healthcare system is that MediSave can be used to pay part of your health insurance premiums.

For most Singaporeans, MediShield Life premiums are fully payable using MediSave. If you have an Integrated Shield Plan, the additional private insurance portion can also be paid using MediSave, up to additional withdrawal limits.

These limits depend on the age of the insured person:

up to SGD 300 per year for those aged 40 and below

up to SGD 600 per year for those aged 41 to 70

up to SGD 900 per year for those aged 71 and above

If your total premium is higher than the MediSave limit, the remaining amount must be paid in cash.

It is also worth noting that rider premiums cannot be paid using MediSave. These are always a cash expense. For many people, this becomes the main ongoing cost of keeping a more comprehensive plan.

Should you buy health insurance?

For many Singaporeans, the more useful question is not whether to buy health insurance, but whether their current coverage is enough for the type of care they would want.

Most people already have a starting layer of protection through MediShield Life. Some also have group insurance through their employer. That may be enough for subsidised treatment in public hospitals or for basic day-to-day care.

However, your current coverage may not be enough if you prefer:

Treatment at a private hospital or higher ward class

Shorter waiting times

More choice over your doctor or specialist

Buying additional health insurance is really about reducing the financial shock of a serious illness or hospital stay. It gives you more options when you need treatment and helps protect your savings from a sudden large bill.

Medical/family history

Your personal health history and family history can affect the type of insurance terms you are offered.

If you have a family history of conditions such as cancer, heart disease, or diabetes, you may understandably worry that this means you will not be covered. In reality, it is usually not that simple.

Having a family history does not automatically mean you will be excluded.

Depending on the insurer’s assessment, you may receive one of the following outcomes:

Standard terms: You are fully covered with no extra premium.

Premium loading: You are still covered, but your premiums are higher (e.g. 20% more) to reflect the insurer’s assessment of risk.

Exclusions: The policy covers most conditions but excludes any specific hereditary conditions that may be linked to your medical or family history.

Insurers assess you based on your health at the time you apply. This is why many advisers recommend getting coverage earlier rather than later. If you develop a condition before applying, that condition may then be excluded or make cover harder to obtain.

What health insurance should you buy?

There is no single best plan for everyone. The right choice depends on your budget, health needs, family situation, and the kind of care you would want if something serious happens.

A practical way to think about it is to start with the most important gap first.

1) Start with hospitalisation cover

If you do not already have an Integrated Shield Plan, this is usually the first area to review.

Ask yourself:

Would you be comfortable staying in a subsidised public ward?

Would you prefer a Class A or B1 ward?

Would you want the option of a private hospital?

How important is specialist choice to you?

Your answers will help guide which IP tier makes sense.

2) Consider Critical Illness cover

An Integrated Shield Plan helps pay medical bills, but it does not replace your income if you are unable to work.

A Critical Illness plan may be worth considering if:

You are the main income earner

You have dependants

Your family would struggle financially if you stopped working for several months

You want a lump sum payout on diagnosis of a covered illness

3) Add Personal Accident cover if relevant

Personal Accident insurance is usually affordable and may be useful if you:

Have an active lifestyle

Work in a physically demanding job

Want added cover for accident-related injuries

4) Choose something sustainable

This is one of the most important points. A plan should not only fit your budget now. It should also remain manageable as premiums rise with age.

It is often better to choose a plan you can keep for the long term than to buy the most expensive option now and feel forced to downgrade later.

How to get started with health insurance

If you have never reviewed your insurance properly, the process can feel confusing at first. The good news is that getting clarity usually starts with a few simple checks.

You do not need to buy anything immediately. The first step is simply to understand what you already have.

Once you have this information, it becomes much easier to see whether there are any major gaps.

Assessing your current coverage

Before looking at new plans, review your existing coverage carefully.

You can sign in to the CPF Healthcare Dashboard via Singpass to check your current health insurance arrangements. This will show whether you have an Integrated Shield Plan and which insurer is providing it.

If you are working, it is also worth checking your company health benefits. Ask your HR department for a summary of benefits if needed.

Pay attention to the following:

Ward class or hospital setting covered

Whether pre- and post-hospitalisation benefits are included

Whether panel doctors apply

What your deductible and co-insurance are

Whether a rider is attached

What happens if you leave your job

A lot of people assume they are well covered until they look more closely. Even a short review can highlight important gaps.

Questions to ask before buying

If you are considering a new policy, it helps to go into the discussion with a few clear questions.

Ask the adviser or insurer:

What is the exact deductible and co-insurance for my chosen ward class, and what is my maximum out-of-pocket exposure per year with and without a rider?

Are there any exclusions on this policy based on my current health or medical history?

Which doctors and specialists are on the panel for this plan, and what happens to my coverage if I see someone outside the panel?

How have premiums for this plan changed over the past five years, and what should I expect them to look like at ages 60 and 70?

A good adviser should be able to explain these clearly and without rushing you. Take your time with the process and compare your options side by side. If something still feels unclear, it is reasonable to compare a few options before making a decision.

This article is intended for informational purposes only and does not constitute financial or legal advice. Thomson Medical does not earn any commission, referral fees, or financial benefit from any insurance products or providers mentioned in this article. All information is provided purely to help you better understand Singapore's health insurance landscape.

Individual circumstances vary, and the right insurance plan depends on your personal health profile, financial situation, and coverage needs. Before making any decisions about your health insurance, we strongly recommend speaking with a licensed financial adviser or your insurance provider directly. Alternatively, you may reach out to our medical concierge should you require any assistance.

FAQs

Can I seek treatment outside of my insurance panel?

Yes, but it will cost you more. Most IPs offer full benefits, including pre-authorisation and lower co-payments, when you stay within your insurer's panel. Going outside the panel means higher out-of-pocket costs and fewer benefits. Some insurers offer an Extended Panel option as a middle ground, so check with your insurer before assuming you have to choose between panel and fully private.

What actually happens if I get seriously ill and my hospital bill is more than my IP's annual claim limit? Who pays the rest?

You pay the remainder out of pocket. This is most likely to happen with complex or prolonged treatments such as cancer, where costs accumulate across multiple hospital stays. To reduce this risk, choose an IP with a high annual claim limit and check whether your plan includes enhanced cancer drug coverage.

I have a pre-existing condition. Does that mean I cannot get an Integrated Shield Plan, or will it just be excluded from my coverage?

Not necessarily. Insurers assess your application through a process called underwriting. Depending on your condition and how well it is managed, they may cover you with that condition excluded, charge a higher premium, or in some cases decline the application. Outcomes vary between insurers, so it is worth approaching more than one before drawing conclusions.

My IP covers private hospitals but I always end up going to a public hospital anyway. Am I wasting money on a plan I never actually use?

If you consistently choose public hospitals despite having a private hospital IP, you might be paying for coverage you’re not using. A lower-tier plan covering Class A or B1 wards at public hospitals may give you adequate coverage at a lower premium.

With the new IP rider changes from April 2026, does that mean I will have to pay more out of pocket when I am hospitalised? How much more?

For policyholders who purchase new riders from April 2026 onwards, yes, the out-of-pocket exposure will be higher than under the previous full rider structure. The key changes are that new riders will no longer be permitted to cover the minimum IP deductible set by MOH, which ranges from $1,500 to $3,500 depending on your ward class, and the annual co-payment cap has been raised from $3,000 to $6,000. This means that for a hospitalisation at a private hospital, you could be responsible for the deductible amount plus up to $6,000 in co-payments within a single policy year, before your insurer covers the rest. If you already hold a rider purchased before 27 November 2025, your existing terms remain in place until at least your policy renewal after 1 April 2028, giving you time to assess whether transitioning to a new rider structure makes financial sense for your situation.

Do I actually need Critical Illness insurance on top of my IP, or is that just another upsell?

They cover different things. An IP pays your hospital bills. A CI plan pays you directly, as a lump sum, when you are diagnosed with a serious illness. That money can replace lost income, cover mortgage payments, or fund costs your IP does not reimburse. If a prolonged period without income would put real strain on your finances, a CI plan fills a gap your IP cannot.

If I switch insurers to get a lower premium, will my new insurer cover conditions that my current insurer was already covering?

Not necessarily. Switching triggers fresh underwriting, so any conditions that developed since your original policy was taken out may be excluded by the new insurer. If your health has not changed since you first applied, switching is lower risk. If it has, the savings on premiums may not be worth the gaps you take on.

My parents are getting older and I am worried about their medical bills. Can I use my MediSave to pay for their health insurance premiums, and are there limits on how much I can contribute?

Yes, you can use your MediSave to pay for the MediShield Life and Integrated Shield Plan premiums of your immediate family members, including parents. The amount you can contribute from MediSave towards a family member's IP is subject to the same Additional Withdrawal Limits that apply to your own plan.

Is company health insurance / group health insurance enough?

Not on its own. Group coverage is tied to your employment, so it stops the moment you leave your job. If you develop a health condition while relying solely on your employer's plan, a new insurer may treat it as pre-existing when you apply for individual coverage later, which can lead to exclusions, higher premiums, or a declined application. Think of group insurance as a useful supplement, not a substitute for your own plan.

For more information, contact us:

Thomson Medical Concierge

- 8.30am - 5.30pm

- WhatsApp: 9147 2051

Need help finding the right specialist or booking for a group?

Our Medical Concierge is here to help you. Simply fill in our form, and we'll check and connect you with the right specialist promptly.

Notice:

The range of services may vary between Thomson clinic locations. Please contact your preferred branch directly to enquire about the current availability.

Get In Touch